2012-06-22 15:11:52

ΠΗΓΗ: FT

by Gavyn Davies

Another week, another summit. Once again, we are being told, this time by Italian prime minister Mario Monti, that there is only one week left to save the euro. Yet the crisis still does not seem sufficiently acute to persuade eurozone leaders that a full resolution is necessary.

The next summit on June 28 and 29 will unveil a long term road map towards fiscal and banking union, which in better economic circumstances could appear highly impressive. But the market is currently focused on the shorter term. Unless there is some form of debt mutualisation at the summit, resulting in a decline in government bond yields in Spain and Italy, the crisis could rapidly worsen.

Debt mutualisation can come in many forms. The European Redemption Fund, proposed by the Council of Economic Experts in Germany (and discussed here) seems to have receded into the background this week but could still have an eventual role. More immediately, the main option on the table seems to be the use of the eurozone firewall (ie a combination of the EFSF and ESM) to buy secondary government debt, or inject capital directly to the banks. But the problem here is simple: a lack of money.

So far, the EFSF has lent €248bn of its original €440bn lending capacity. At the end of this month, the ESM treaty is supposed to be ratified, and the entity will become immediately operational with a maximum lending capacity of €500bn. However, there have been problems with ratification in several member states, including Germany, where the legal challenge being brought by the Left at the constitutional court could take a while to resolve.

This is not necessarily fatal, however, because the EFSF can fill the breach by undertaking new lending up to July 2013. The key is that the EFSF and the ESM together can lend an additional €500bn from now on. If the EFSF does more in the next 12 months, the ESM will have less money available later.

The first call on this money will be the €100bn which will be disbursed for the Spanish bank bail out. That €100bn will presumably need to come out of the total €500bn of new lending capacity, leaving €400bn for other purposes. Germany has been very insistent on maintaining the €500bn ceiling, because this sets a limit on its potential losses from this form of debt mutualisation. There is no sign of this changing.

If unleveraged, this €400bn looks like a very small number, compared with the financing needs of Spain and Italy in the next couple of years. It used to be said in the markets that the eurozone firewall might just be large enough to deal with a loss of market access for Spain, but would not be large enough to deal with Italy as well. That assessment could turn out to be too optimistic. The arithmetic of eurozone government refinancing needs, relative to the size of the current firewall, looks increasingly unpleasant.

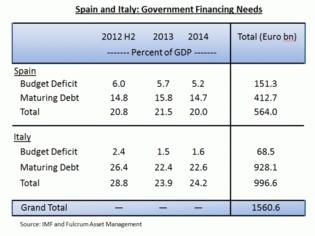

In Spain, government refinancing needs up to the end of 2014 amount to around €564bn, or 52 per cent of a single year’s GDP. Of this, around one quarter stems from the budget deficit, while three quarters stems from maturing debt. Maturing debt is normally easier to refinance, because bond managers re-allocate the money they receive from redemptions back into the bond market. But that can quickly change during a crisis, when bond managers typically sit on their hands rather than reinvesting their cash. Spain has not yet lost market access, but is in danger of doing so.

Italy is different. Total refinancing needs up to the end of 2014 amount to €997bn, but 93 per cent of those needs stem from maturing debt. The primary budget surplus in Italy is a very strong defence against a market crisis, but not necessarily a sufficient defence if there are increasing fears of a euro break-up. Former prime minister Silvio Berlusconi’s flirtation with a return to the lira this week will not help scotch these fears.

Overall, the remaining €400bn firepower in the EFSF/ESM is probably inadequate to finance a bail-out programme for Spain, and would of course be dwarfed by the €1,600 bn needed for both Spain and Italy. In the near term, what this means is that there is very little spare money in the EFSF/ESM to initiate a bond buying programme in the secondary market, which was the favoured option in the G20 summit discussions this week.

If the EFSF/ESM uses its lending capacity in the near future to support Spanish and Italian secondary bond markets, it will rapidly absorb funds which might soon be needed for a Spanish debt programme. The IMF will hopefully be able to contribute to such a programme, but the attitude of the US to providing more financial support for the eurozone ahead of the Presidential election could be very hostile. Without IMF money, the arithmetic gets even more difficult. The markets can do arithmetic, and would quickly realise that a programme of secondary bond purchases would have inadequate firepower to restore confidence.

Increasing the lending capacity of the ESM, before it has even been ratified, in the current German political climate, is a non-starter. Leveraging the effective size of the EFSF/ESM by providing first tranche loss insurance to private bond investors has already been tried after previous summits, without any obvious success. That leaves one very familiar final option, which is a further use of the ECB balance sheet.

So we will probably see more debt mutualisation via the activities of the ECB. This could occur in several different flavours: outright bond purchases through the central bank’s Securities Markets Programme; allowing the ECB to provide leverage to the ESM; or further LTROs to encourage banks to hold more government debt. The ECB probably does not like any of this, but may well prefer the second and third flavours to the first.

Once again, it is all up to Mario Draghi.

youpayyourcrisis

by Gavyn Davies

Another week, another summit. Once again, we are being told, this time by Italian prime minister Mario Monti, that there is only one week left to save the euro. Yet the crisis still does not seem sufficiently acute to persuade eurozone leaders that a full resolution is necessary.

The next summit on June 28 and 29 will unveil a long term road map towards fiscal and banking union, which in better economic circumstances could appear highly impressive. But the market is currently focused on the shorter term. Unless there is some form of debt mutualisation at the summit, resulting in a decline in government bond yields in Spain and Italy, the crisis could rapidly worsen.

Debt mutualisation can come in many forms. The European Redemption Fund, proposed by the Council of Economic Experts in Germany (and discussed here) seems to have receded into the background this week but could still have an eventual role. More immediately, the main option on the table seems to be the use of the eurozone firewall (ie a combination of the EFSF and ESM) to buy secondary government debt, or inject capital directly to the banks. But the problem here is simple: a lack of money.

So far, the EFSF has lent €248bn of its original €440bn lending capacity. At the end of this month, the ESM treaty is supposed to be ratified, and the entity will become immediately operational with a maximum lending capacity of €500bn. However, there have been problems with ratification in several member states, including Germany, where the legal challenge being brought by the Left at the constitutional court could take a while to resolve.

This is not necessarily fatal, however, because the EFSF can fill the breach by undertaking new lending up to July 2013. The key is that the EFSF and the ESM together can lend an additional €500bn from now on. If the EFSF does more in the next 12 months, the ESM will have less money available later.

The first call on this money will be the €100bn which will be disbursed for the Spanish bank bail out. That €100bn will presumably need to come out of the total €500bn of new lending capacity, leaving €400bn for other purposes. Germany has been very insistent on maintaining the €500bn ceiling, because this sets a limit on its potential losses from this form of debt mutualisation. There is no sign of this changing.

If unleveraged, this €400bn looks like a very small number, compared with the financing needs of Spain and Italy in the next couple of years. It used to be said in the markets that the eurozone firewall might just be large enough to deal with a loss of market access for Spain, but would not be large enough to deal with Italy as well. That assessment could turn out to be too optimistic. The arithmetic of eurozone government refinancing needs, relative to the size of the current firewall, looks increasingly unpleasant.

In Spain, government refinancing needs up to the end of 2014 amount to around €564bn, or 52 per cent of a single year’s GDP. Of this, around one quarter stems from the budget deficit, while three quarters stems from maturing debt. Maturing debt is normally easier to refinance, because bond managers re-allocate the money they receive from redemptions back into the bond market. But that can quickly change during a crisis, when bond managers typically sit on their hands rather than reinvesting their cash. Spain has not yet lost market access, but is in danger of doing so.

Italy is different. Total refinancing needs up to the end of 2014 amount to €997bn, but 93 per cent of those needs stem from maturing debt. The primary budget surplus in Italy is a very strong defence against a market crisis, but not necessarily a sufficient defence if there are increasing fears of a euro break-up. Former prime minister Silvio Berlusconi’s flirtation with a return to the lira this week will not help scotch these fears.

Overall, the remaining €400bn firepower in the EFSF/ESM is probably inadequate to finance a bail-out programme for Spain, and would of course be dwarfed by the €1,600 bn needed for both Spain and Italy. In the near term, what this means is that there is very little spare money in the EFSF/ESM to initiate a bond buying programme in the secondary market, which was the favoured option in the G20 summit discussions this week.

If the EFSF/ESM uses its lending capacity in the near future to support Spanish and Italian secondary bond markets, it will rapidly absorb funds which might soon be needed for a Spanish debt programme. The IMF will hopefully be able to contribute to such a programme, but the attitude of the US to providing more financial support for the eurozone ahead of the Presidential election could be very hostile. Without IMF money, the arithmetic gets even more difficult. The markets can do arithmetic, and would quickly realise that a programme of secondary bond purchases would have inadequate firepower to restore confidence.

Increasing the lending capacity of the ESM, before it has even been ratified, in the current German political climate, is a non-starter. Leveraging the effective size of the EFSF/ESM by providing first tranche loss insurance to private bond investors has already been tried after previous summits, without any obvious success. That leaves one very familiar final option, which is a further use of the ECB balance sheet.

So we will probably see more debt mutualisation via the activities of the ECB. This could occur in several different flavours: outright bond purchases through the central bank’s Securities Markets Programme; allowing the ECB to provide leverage to the ESM; or further LTROs to encourage banks to hold more government debt. The ECB probably does not like any of this, but may well prefer the second and third flavours to the first.

Once again, it is all up to Mario Draghi.

youpayyourcrisis

ΜΟΙΡΑΣΤΕΙΤΕ

ΔΕΙΤΕ ΑΚΟΜΑ

ΠΡΟΗΓΟΥΜΕΝΟ ΑΡΘΡΟ

Δείτε ποιά ζώδια ερωτεύονται τα φιλαράκια τους!

ΣΧΟΛΙΑΣΤΕ