2012-03-21 10:08:08

COSTA NAVARINO is a luxury resort in the south-western Peloponnese, a 270km (168-mile) drive from Athens. It has two large luxury hotels, an assortment of pricey homes, a sports centre, some posh shops and two golf courses, one designed by Bernhard Langer, a German golf star of the 1980s and 1990s. The well-heeled traveller looking for more than a beach holiday can also choose from watersports, bird-watching or guided nature walks.It is a world away from the austerity and social tension that is gripping most of Greece. Yet any long-term revival in the Greek economy hinges on this sort of enterprise. Around 15% of Greek GDP comes directly or indirectly from tourism, according to McKinsey, a consultancy. But tourism, like other Greek industries, is short of the kind of large developments, such as Costa Navarino, that can reap economies of scale and squeeze more year-round revenue from each euro invested.

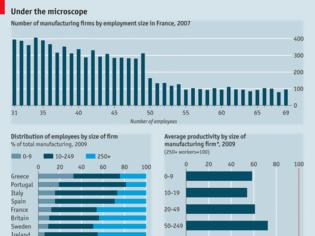

Greece stands out among European Union countries as having the most stunted firms. Around a third of Greek manufacturers are “micro” firms with fewer than ten workers, compared with 4.3% of firms in Germany (see left-hand chart). But the small-firm problem also afflicts the other troubled economies at the euro zone’s southern periphery. Spain lacks biggish manufacturers; Italy’s small-firm bias derives in part from a reverence for family firms. Only 19% of Portuguese manufacturers have 250 or more workers, compared with 55% of industrial firms in Germany. “The incredible shrinking Portuguese firm” is the title of a research paper* by three economists at Carnegie Mellon University, which shows that Portugal had more small firms and fewer big ones in 2009 than it had in the 1980s. The authors find the trend has been towards larger firms in America, as well as in Denmark, a country of comparable size to Portugal.A bias to small firms is costly. The productivity of European firms with fewer than 20 workers is on average little more than half that of firms with 250 or more workers (see right-hand chart). The deeper roots of the euro-zone crisis lie with the loss of competitiveness in the region’s trouble spots. This problem owes more to dismal productivity growth in the past decade than to rapid wage inflation. If the best small firms were able to grow bigger, Greece and the rest might solve their competitiveness problems without having to cut wages or leave the euro.The periphery’s productivity malaise is the result of the rigid rules that govern jobs and goods markets. In theory the key to prosperity is the amount of physical capital and skilled workers in an economy, and how they are combined. But the quality of companies will vary so it matters greatly where—as well as how well and how much—capital and skills are deployed. If restrictive rules mean that resources are trapped in inefficient firms, it leaves the best companies starved of them. The result is sluggish productivity. The Carnegie Mellon economists blame Portugal’s shrinking firms on its employment laws, which are among the strictest in the OECD (though becoming more forgiving) and act as a tax on firm size, because small firms are sheltered from them.Growth hormones wantedEstablishing a direct link between regulation and firm size is tricky, as different rules apply at different-sized thresholds. In France, however, lots of rules kick in once firms employ 50 workers. A study* by Luis Garicano, Claire LeLarge and John Van Reenen of the London School of Economics (LSE) uses this boundary to test whether French manufacturers are kept small by regulation, and found a steep fall in firms with precisely 50 workers (see top chart). The bunching before this mark suggests that firms that might have grown bigger chose to stay small.The barriers to growing are far higher in Greece, one of Europe’s most regulated economies. In addition to rigid jobs rules, its licensing set-up is almost comically cumbersome. It can take visits to ten or more bureaus at several ministries and the filing of dozens of documents to get final approval for a business plan. Restrictions on land use keep Greek ventures from quickly reaching an efficient scale. It took 30 years for developers to assemble the plots for the Costa Navarino resort; little wonder that most Greek hotels have fewer than 100 rooms. Land-use restrictions are a problem in retailing, too. Greece has almost double the number of shops per head as the western European average, says McKinsey. As a consequence, Greek stores yield 40% less output than they might from each square foot of retail space.The prescription for Greece and others is a familiar one: relaxing the rules that govern jobs, wages and land development will allow the best enterprises to grow bigger and the duds to fail, boosting productivity, GDP growth and tax revenues. Yet the idea that small firms are best persists even in less regulated places, such as America and Britain. This fixation owes much to the idea that small businesses create the most jobs. But a study by John Haltiwanger of the University of Maryland, with two researchers at the US Census Bureau, finds that young firms, most of which happen to be small, account for much of America’s jobs growth. Mature small firms often destroy jobs, as do small start-ups that do not survive. It is better to be young than petite.

Sources"The Incredible Shrinking Portuguese Firm", by Serguey Braguinsky, Lee G Branstetter and Andre Regateiro, NBER working paper No. 17265, July 2011"Firm Size Distortions and the Productivity Distribution: Evidence from France", by Luis Garicano, Claire LeLarge and John Van Reenen, Centre for Economic Performance discussion paper No. 1128, February 2012"Who Creates Jobs? Small vs Large vs Young", by John C Haltiwanger, Ron S Jarmin and Javier Miranda, NBER working paper No. 16300, August 2010"Greece Ten Years Ahead: Defining Greece's New Growth Model and Strategy", McKinsey & Company, Athens Office, November 2011

Economist.com/blogs/freeexchangeECONOMIST

Greece stands out among European Union countries as having the most stunted firms. Around a third of Greek manufacturers are “micro” firms with fewer than ten workers, compared with 4.3% of firms in Germany (see left-hand chart). But the small-firm problem also afflicts the other troubled economies at the euro zone’s southern periphery. Spain lacks biggish manufacturers; Italy’s small-firm bias derives in part from a reverence for family firms. Only 19% of Portuguese manufacturers have 250 or more workers, compared with 55% of industrial firms in Germany. “The incredible shrinking Portuguese firm” is the title of a research paper* by three economists at Carnegie Mellon University, which shows that Portugal had more small firms and fewer big ones in 2009 than it had in the 1980s. The authors find the trend has been towards larger firms in America, as well as in Denmark, a country of comparable size to Portugal.A bias to small firms is costly. The productivity of European firms with fewer than 20 workers is on average little more than half that of firms with 250 or more workers (see right-hand chart). The deeper roots of the euro-zone crisis lie with the loss of competitiveness in the region’s trouble spots. This problem owes more to dismal productivity growth in the past decade than to rapid wage inflation. If the best small firms were able to grow bigger, Greece and the rest might solve their competitiveness problems without having to cut wages or leave the euro.The periphery’s productivity malaise is the result of the rigid rules that govern jobs and goods markets. In theory the key to prosperity is the amount of physical capital and skilled workers in an economy, and how they are combined. But the quality of companies will vary so it matters greatly where—as well as how well and how much—capital and skills are deployed. If restrictive rules mean that resources are trapped in inefficient firms, it leaves the best companies starved of them. The result is sluggish productivity. The Carnegie Mellon economists blame Portugal’s shrinking firms on its employment laws, which are among the strictest in the OECD (though becoming more forgiving) and act as a tax on firm size, because small firms are sheltered from them.Growth hormones wantedEstablishing a direct link between regulation and firm size is tricky, as different rules apply at different-sized thresholds. In France, however, lots of rules kick in once firms employ 50 workers. A study* by Luis Garicano, Claire LeLarge and John Van Reenen of the London School of Economics (LSE) uses this boundary to test whether French manufacturers are kept small by regulation, and found a steep fall in firms with precisely 50 workers (see top chart). The bunching before this mark suggests that firms that might have grown bigger chose to stay small.The barriers to growing are far higher in Greece, one of Europe’s most regulated economies. In addition to rigid jobs rules, its licensing set-up is almost comically cumbersome. It can take visits to ten or more bureaus at several ministries and the filing of dozens of documents to get final approval for a business plan. Restrictions on land use keep Greek ventures from quickly reaching an efficient scale. It took 30 years for developers to assemble the plots for the Costa Navarino resort; little wonder that most Greek hotels have fewer than 100 rooms. Land-use restrictions are a problem in retailing, too. Greece has almost double the number of shops per head as the western European average, says McKinsey. As a consequence, Greek stores yield 40% less output than they might from each square foot of retail space.The prescription for Greece and others is a familiar one: relaxing the rules that govern jobs, wages and land development will allow the best enterprises to grow bigger and the duds to fail, boosting productivity, GDP growth and tax revenues. Yet the idea that small firms are best persists even in less regulated places, such as America and Britain. This fixation owes much to the idea that small businesses create the most jobs. But a study by John Haltiwanger of the University of Maryland, with two researchers at the US Census Bureau, finds that young firms, most of which happen to be small, account for much of America’s jobs growth. Mature small firms often destroy jobs, as do small start-ups that do not survive. It is better to be young than petite.

Sources"The Incredible Shrinking Portuguese Firm", by Serguey Braguinsky, Lee G Branstetter and Andre Regateiro, NBER working paper No. 17265, July 2011"Firm Size Distortions and the Productivity Distribution: Evidence from France", by Luis Garicano, Claire LeLarge and John Van Reenen, Centre for Economic Performance discussion paper No. 1128, February 2012"Who Creates Jobs? Small vs Large vs Young", by John C Haltiwanger, Ron S Jarmin and Javier Miranda, NBER working paper No. 16300, August 2010"Greece Ten Years Ahead: Defining Greece's New Growth Model and Strategy", McKinsey & Company, Athens Office, November 2011

Economist.com/blogs/freeexchangeECONOMIST

ΜΟΙΡΑΣΤΕΙΤΕ

ΔΕΙΤΕ ΑΚΟΜΑ

ΠΡΟΗΓΟΥΜΕΝΟ ΑΡΘΡΟ

"Γουστάρω την Τούμπα!"

ΣΧΟΛΙΑΣΤΕ

![Παγκόσμια ημέρα για το Σύνδρομο Down 2012 - Μύθοι και αλήθειες [video]](https://images.newsnowgreece.com/2/23892/pagkosmia-imera-gia-to-syndromo-Down-2012---mythoi-kai-alitheies-video-1-124x78.jpg)