2016-04-25 00:45:19

Matt O'Brien looks at Greece's debt deal, and what might happen next.

https://www.weforum.org/

Matt O'BrienReporter, Washington Post

IMF wants Greece to do less austerity, and Greece wants to do more as long as those cuts don't hit the poor. !!??

Sometimes it's hard to tell whether history is repeating itself as tragedy or as farce.

Greece, after all, has had plenty of both over the past eight years. Its economy has shrunk as much as the United States' did during the Great Depression, its government has collapsed over and over and over again as a result, and its bailout is in its third iteration — without which it would have been forced out of the euro zone. How bad are things? Greek Prime Minister Alexis Tsipras just touted the fact that his country's unemployment rate has fallen from 26.5 percent to 24.9 percent, and that there was a month last year in which Greece's industrial production grew faster than anyone else's in Europe.

When life doesn't even give you lemons, you have to pick cherries instead.

Greece might not even be able to do that, though, if it starts fighting over its bailout terms again. That would bring back the fear that it wasn't going to stay in the euro zone, and, consequently, the incentive for people to pull all of their euros out of the country's banks before they could get turned into drachmas that wouldn't be worth anywhere near as much. Its underwhelming recovery would become none at all.

Image: BBC

And that brings us to the bad news. Greece is, in fact, squabbling with the International Monetary Fund over the bailout that the two of them and the European Commission agreed to agree to last year. But — this is where it's hard to tell tragedy from farce — it's not for the reason you might think. It's the IMF that wants Greece to do less austerity, and Greece that wants to do more as long as those cuts don't hit the poor. In other words, up is down, black is white, and dogs and cats really are living together.

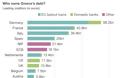

But let's back up a minute. How did Greece get here in the first place? Easy: its government spent too much during the boom, but its creditors have forced it to cut too much during the bust without giving it any way to grow. That means it not only has a big pile of debt to pay back, but also that it's less able to do so since its economy is so much smaller — about 25 percent in total — than it used to be. That's how you get debt that's 179 percent of your gross domestic product.

Now, Europe's dirty little not-so-secret is that Greece is never going to pay all this back. It'd need a lot more inflation for that to happen, which isn't a possibility as long as it's part of the euro zone. But politicians, of course, can't exactly say that. So instead, they've resorted to a pair of lies: that Greece can and will pay back its debt. And that's where things get tricky. To maintain this fiction, Greece has needed one bailout after another to be able to pay back what it owes today, and put on one austerity budget after another to be able to pay back what it owes tomorrow — or at least say that with something resembling a straight face.

The question, then, is how believable this second part is. The IMF doesn't think it is at all. Consider this: Greece is supposed to push through big tax hikes and spending cuts that, excluding its interest payments, will get it to a surplus of 3.5 percent of gross domestic product by 2018 — and then stay there for decades. But the problem with that, as economists Barry Eichengreen and Ugo Panizzapoint out, is that barely any countries have been able to do something like that for 10 years, let alone 20 or 30. It would take, as IMF Managing Director Christine Lagarde puts it, a "heroic" effort just to hit this target for the next few years, but it's "highly unrealistic" to think that it could "maintained for decades."

Here's the easiest way to think about what's going on. There are three sides to these bailout talks, and three totally different set of priorities. Greece cares, in this order, about: 1) getting its debt written down, 2) keeping any cuts from striking its poorest people, and 3) keeping the surplus it's supposed to achieve as small as possible. The cynical — or is it sensible? — idea is that since their lenders will never forgive any of their debt, it's better to focus on minimizing pension cuts that will always hurt rather than budget targets that can be always be missed.

The IMF, meanwhile, is focused on: 1) keeping the surplus Greece is supposed to run asrealistic as possible, 2) getting some of its debt written down, and 3) insofar as it doesn't conflict with this first goal, keeping any cuts from being unnecessarily regressive. The simple story is that the IMF is tired of giving its imprimatur to deals it knows won't work, as it all but admitted was the case with the first Greek bailout. That means today's cuts must be kept at a reasonable level, and the debt must be too so that tomorrow's are as well. And while nobody wants to put even this smaller burden on the poor, what will help the most, the IMF says, is a program that works and an economy that's growing.

Then there's the European Commission, which is basically Germany. Its objective is: 1) notwriting down Greece's debt, 2) keeping the surplus Greece is supposed to engineer as large as possible, and 3) keeping any cuts from harming the most vulnerable. In their view, they'vealready done a lot to reduce Greece's debt burden — which is what matters more than the debt level — by refinancing it at rock-bottom rates and giving Athens decades rather than years to pay it all back. Going further by reducing the face value of the debt would, they say, be too much. Their voters would revolt. The same would supposedly happen if Greece was allowed to run a smaller surplus. That would lay bare the fantasy that it would ever pay back what it owes. But, at the same time, Germany doesn't have a big problem with Greece doing austerity the way it likes as long as it's the amount of austerity it's told to do.

You'd think that Greece and the IMF would be allies here. Both of them, after all, want more debt and austerity relief. But that's not what's happened. Believe it or not, Greece is actually denouncing the IMF for saying that it should only shoot for a primary surplus of 1.5 percent of 3.5 percent of GDP in 2018. Why is that? Well, the disagreement comes down to this: the IMF thinks Greece's proposed tax hikes go too far, and its pension cuts don't go far enough. So even though it wants Greece to do less austerity overall, it wants Greece to do more of the kind of austerity that Greece doesn't want to do. And Athens, for its part, would rather keep what it thinks would be the social harm to a minimum rather than the economic harm. So the upshot is that Greece is siding with the people who want it to cut more, but never want to cut its debt. At least they'll let Greece slash the deficit the way it wants to.

In the second-worst case, this would make the IMF walk away from the deal, and it would fall apart. But even worse than that is what's actually going to happen. They'll all agree to some kind of fudge, and then, when that doesn't work, negotiate a new one a few years from now. At that rate, though, it might be another 8 to 10 years before Greece's economy is back to being as big as it was in 2008.

It's enough to make you cry till you laugh or laugh till you cry.

medispin

https://www.weforum.org/

Matt O'BrienReporter, Washington Post

IMF wants Greece to do less austerity, and Greece wants to do more as long as those cuts don't hit the poor. !!??

Sometimes it's hard to tell whether history is repeating itself as tragedy or as farce.

Greece, after all, has had plenty of both over the past eight years. Its economy has shrunk as much as the United States' did during the Great Depression, its government has collapsed over and over and over again as a result, and its bailout is in its third iteration — without which it would have been forced out of the euro zone. How bad are things? Greek Prime Minister Alexis Tsipras just touted the fact that his country's unemployment rate has fallen from 26.5 percent to 24.9 percent, and that there was a month last year in which Greece's industrial production grew faster than anyone else's in Europe.

When life doesn't even give you lemons, you have to pick cherries instead.

Greece might not even be able to do that, though, if it starts fighting over its bailout terms again. That would bring back the fear that it wasn't going to stay in the euro zone, and, consequently, the incentive for people to pull all of their euros out of the country's banks before they could get turned into drachmas that wouldn't be worth anywhere near as much. Its underwhelming recovery would become none at all.

Image: BBC

And that brings us to the bad news. Greece is, in fact, squabbling with the International Monetary Fund over the bailout that the two of them and the European Commission agreed to agree to last year. But — this is where it's hard to tell tragedy from farce — it's not for the reason you might think. It's the IMF that wants Greece to do less austerity, and Greece that wants to do more as long as those cuts don't hit the poor. In other words, up is down, black is white, and dogs and cats really are living together.

But let's back up a minute. How did Greece get here in the first place? Easy: its government spent too much during the boom, but its creditors have forced it to cut too much during the bust without giving it any way to grow. That means it not only has a big pile of debt to pay back, but also that it's less able to do so since its economy is so much smaller — about 25 percent in total — than it used to be. That's how you get debt that's 179 percent of your gross domestic product.

Now, Europe's dirty little not-so-secret is that Greece is never going to pay all this back. It'd need a lot more inflation for that to happen, which isn't a possibility as long as it's part of the euro zone. But politicians, of course, can't exactly say that. So instead, they've resorted to a pair of lies: that Greece can and will pay back its debt. And that's where things get tricky. To maintain this fiction, Greece has needed one bailout after another to be able to pay back what it owes today, and put on one austerity budget after another to be able to pay back what it owes tomorrow — or at least say that with something resembling a straight face.

The question, then, is how believable this second part is. The IMF doesn't think it is at all. Consider this: Greece is supposed to push through big tax hikes and spending cuts that, excluding its interest payments, will get it to a surplus of 3.5 percent of gross domestic product by 2018 — and then stay there for decades. But the problem with that, as economists Barry Eichengreen and Ugo Panizzapoint out, is that barely any countries have been able to do something like that for 10 years, let alone 20 or 30. It would take, as IMF Managing Director Christine Lagarde puts it, a "heroic" effort just to hit this target for the next few years, but it's "highly unrealistic" to think that it could "maintained for decades."

Here's the easiest way to think about what's going on. There are three sides to these bailout talks, and three totally different set of priorities. Greece cares, in this order, about: 1) getting its debt written down, 2) keeping any cuts from striking its poorest people, and 3) keeping the surplus it's supposed to achieve as small as possible. The cynical — or is it sensible? — idea is that since their lenders will never forgive any of their debt, it's better to focus on minimizing pension cuts that will always hurt rather than budget targets that can be always be missed.

The IMF, meanwhile, is focused on: 1) keeping the surplus Greece is supposed to run asrealistic as possible, 2) getting some of its debt written down, and 3) insofar as it doesn't conflict with this first goal, keeping any cuts from being unnecessarily regressive. The simple story is that the IMF is tired of giving its imprimatur to deals it knows won't work, as it all but admitted was the case with the first Greek bailout. That means today's cuts must be kept at a reasonable level, and the debt must be too so that tomorrow's are as well. And while nobody wants to put even this smaller burden on the poor, what will help the most, the IMF says, is a program that works and an economy that's growing.

Then there's the European Commission, which is basically Germany. Its objective is: 1) notwriting down Greece's debt, 2) keeping the surplus Greece is supposed to engineer as large as possible, and 3) keeping any cuts from harming the most vulnerable. In their view, they'vealready done a lot to reduce Greece's debt burden — which is what matters more than the debt level — by refinancing it at rock-bottom rates and giving Athens decades rather than years to pay it all back. Going further by reducing the face value of the debt would, they say, be too much. Their voters would revolt. The same would supposedly happen if Greece was allowed to run a smaller surplus. That would lay bare the fantasy that it would ever pay back what it owes. But, at the same time, Germany doesn't have a big problem with Greece doing austerity the way it likes as long as it's the amount of austerity it's told to do.

You'd think that Greece and the IMF would be allies here. Both of them, after all, want more debt and austerity relief. But that's not what's happened. Believe it or not, Greece is actually denouncing the IMF for saying that it should only shoot for a primary surplus of 1.5 percent of 3.5 percent of GDP in 2018. Why is that? Well, the disagreement comes down to this: the IMF thinks Greece's proposed tax hikes go too far, and its pension cuts don't go far enough. So even though it wants Greece to do less austerity overall, it wants Greece to do more of the kind of austerity that Greece doesn't want to do. And Athens, for its part, would rather keep what it thinks would be the social harm to a minimum rather than the economic harm. So the upshot is that Greece is siding with the people who want it to cut more, but never want to cut its debt. At least they'll let Greece slash the deficit the way it wants to.

In the second-worst case, this would make the IMF walk away from the deal, and it would fall apart. But even worse than that is what's actually going to happen. They'll all agree to some kind of fudge, and then, when that doesn't work, negotiate a new one a few years from now. At that rate, though, it might be another 8 to 10 years before Greece's economy is back to being as big as it was in 2008.

It's enough to make you cry till you laugh or laugh till you cry.

medispin

ΦΩΤΟΓΡΑΦΙΕΣ

ΜΟΙΡΑΣΤΕΙΤΕ

ΔΕΙΤΕ ΑΚΟΜΑ

![Χίλια μπράβο! Δεν έχει δάχτυλα αλλά αυτό δεν τον εμπόδισε να γίνει πιανίστας και μάλιστα από τους καλύτερους... [video]](https://images.newsnowgreece.com/92/924762/xilia-mpravo-den-exei-daxtyla-alla-afto-den-ton-empodise-na-ginei-pianistas-kai-malista-apo-tous-kalyterous-video-1-124x78.jpg)

ΣΧΟΛΙΑΣΤΕ