2012-04-05 18:25:49

Turkey has one of the world’s zippiest economies, but it is too reliant on hot money ANKARA AND ISTANBUL | from the print editionVISITORS to the top of the Galata Tower in Istanbul are treated to a panoramic view of the old town across the Bosphorus. Originally a wooden lighthouse dating from the sixth century, the tower was rebuilt from stone in 1348 by Genoese merchants. It is an enduring symbol of the benefits of foreign capital to Turkey.

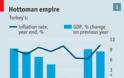

In this section»Istanbuls and bearsClear and present dangerAll that glistersThe Wenzhou experimentBook-cooking guideFrom Brussels, with shoveHistorysisMarjorie Deane internshipsReprintsRelated topicsBusinessEmerging marketsMonetary PolicyPolitical policyEconomic policyBustling below is a city of 15m that lies at the heart of one of the world’s fastest-growing economies. Figures released on April 2nd showed that Turkey’s GDP rose by 8.5% in 2011 after a 9% increase in 2010 (see chart 1)

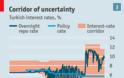

. These are the sort of growth rates that mighty China would be pleased with. Jim O’Neill of Goldman Sachs, who coined the acronym BRIC to denote the big emerging economies of Brazil, Russia, India and China, has included Turkey in MIST, a second tier of biggish rising stars, alongside Mexico, Indonesia and South Korea.But Turkey’s rapid recent growth comes with side-effects that have left its economy vulnerable. One concern is inflation, which was 10.4% in March—well above the central bank’s target and the inflation rates of most of Turkey’s emerging-market peers. A bigger concern is Turkey’s growing dependence on foreign capital to fuel its economy: its current-account deficit averaged 10% of GDP last year (see chart 2). Turkey’s deficit measured in dollars is second only to America’s.More worrying still is that much of the foreign capital that finances Turkey’s current-account deficit is of the flighty sort (flows into banks or purchases of stocks or bonds), which can leave again quickly. Turkey wobbled at the end of last year as worries about the euro zone and its banks intensified. A chunk of Turkey’s banking system is part-owned by banks in the euro-zone periphery and half its exports go to Europe. Net foreign direct investment (FDI) typically accounts for only a small share of capital flows and precious little FDI is new factories or offices. “Before the financial crisis most of Turkey’s FDI was banking deals,” says Murat Ucer of GlobalSource Partners in Istanbul. “Greenfield investment has never been a big part of it.”Enthusiasts brush all this off. Banks are well capitalised, even after a recent surge in credit growth. Public finances are enviable by rich-world standards. Public debt has fallen from 74% of GDP in 2002 to 40% last year. Inflation may be worryingly high but it is a big improvement on the near-70% rate in 2002.Reforms to economic policymaking put in place after a financial crisis in 2001 have made the economy stronger. A recent research paper by Dani Rodrik of Harvard University showed that Turkey’s productivity record improved markedly in the decade after 2000, with average growth rates of 3-3.5% in GDP per person, GDP per worker and industrial output per worker. Income per head (in current dollar prices) has tripled in less than a decade to around $10,000 and there is still plenty of scope for Turkey to converge on the higher living standards of the rich world. Its big domestic market will become bigger: its 75m population is young and is forecast by the United Nations to reach 92m by 2050.Turkey’s location is another selling-point. Its role as a trading post between east and west has been a lure for businessfolk since before the Genoese built the Galata Tower. Today Germany is Turkey’s main trading partner but Iraq, Iran, Egypt, Saudi Arabia and the United Arab Emirates are as important as a block. And these days the merchant class travels by air. Last year Turkish Airlines, a part-privatised carrier, flew 17m international passengers to more than 150 cities. There are plans for a new airport in Istanbul to secure its position as an international hub.Frailty and foreignersYet for all its undoubted strengths, Turkey’s dependence on external financing leaves it prone to volatile cycles governed by the greed and fear of foreigners. Turkey is, in the jargon, a “high-beta” economy. When the outlook for the global economy is brighter or investors are keen to take risks for other reasons, money flows into Turkey in search of high investment returns. That pushes up the lira, encourages spending on imports and widens the current-account deficit. But when investors turn fearful, the hot money is pulled from Turkey more quickly than from other places, forcing the lira down and domestic spending to cool.Near-zero interest rates in the rich world have exacerbated the problem of hot-money flows for those emerging markets, such as Turkey, with high interest rates. Turkey’s central bank, the CBRT, has since 2010 tried to ameliorate these cycles with a new policy framework.Instead of setting monetary policy by reference to a benchmark interest rate, the CBRT employs a wide interest-rate “corridor” (see chart 3). When capital inflows are buoyant, as they were until the summer of 2011, the CBRT cuts its borrowing rate at the bottom of the corridor (the rate it pays on deposits) to discourage hot money and to cap the lira. But when capital flows start to dry up, as they did last autumn when the euro crisis intensified, the central bank stops providing cheap liquidity at its main policy rate. Instead the lending rate at the top of the corridor (analogous to the emergency lending rate that other central banks use) becomes the CBRT’s effective interest rate, helping to support the lira.Critics say the policy is too clever by half. Central-bank policy works best when it provides a benchmark for other interest rates in the economy. But banks cannot be sure what the price of central-bank money will be, making it harder to price loans and set deposit rates. One guide to the monetary-policy stance is the overnight repo rate, a market rate calculated by the Istanbul Stock Exchange. On this gauge interest rates have been volatile and now stand at around 10%.A more serious charge is that the central bank lost sight of its inflation target, in its efforts to manage the lira and because of pressure from Recep Tayyip Erdogan, Turkey’s autocratic prime minister. The CBRT refutes this. “We don’t target a level of the lira but when we see a rapid depreciation we stop providing liquidity,” says Turalay Kenc, the bank’s deputy governor. Much of today’s inflation is down to temporary factors—the weaker lira, a jump in food prices and higher indirect taxes—which will soon drop out of the annual rate, he says. “The objective is the 5% inflation target, which we will hit in mid-2013,” says Mr Kenc. “We could bring down inflation more quickly but that would be costly.”The central bank’s defenders say its unorthodox monetary policy is a brave attempt to deal with a tricky problem—volatile capital flows—that besets many emerging markets. Turkey’s bond yields have been fairly stable, which suggests that investors still trust the central bank to slay inflation. But managing the capital flows on which Turkey depends is too big a job for monetary policy alone.Many analysts reckon the slowdown in credit growth from above 40% in mid-2011 is attributable to interventions by Turkey’s bank regulator, the BRSA, which forced banks to set aside more capital and provisions. The central bank’s policy might even be counter-productive. “When foreign investors don’t understand the policy, they stay away,” says one local analyst.The deeper cause of both the high interest rates that attract hot money to Turkey and the big current-account deficit that creates the need for foreign capital is a shortage of domestic savings. A recent report by the World Bank describes how the growing external deficit reflects a decline in the rate of private-sector saving. Turkey’s economic stability—its stronger job market, sound banks and increasing welfare spending—has given householders even less reason to save for a rainy day, as well as greater access to credit. Other countries with a high-inflation past, such as Brazil, have also struggled to instil a strong saving culture to match that of Asia’s emerging economies.A related problem is the competitiveness of many Turkish businesses, which stay small to avoid onerous regulations and are thus less efficient than they might be. That stops them becoming a source for the components that Turkey’s big, family-owned conglomerates find it cheaper to import. But these problems require policies which will deliver results many years hence. “Reducing the current-account deficit is our number-one challenge and priority,” says Mehmet Simsek, Turkey’s finance minister. “All you can do in the short run is cool the economy and we’re doing what we should be doing.”Many economists believe it would be a prudent short-term course for the public sector to save more (in other words, to run a budget surplus) to make up for the lack of private saving. That would cut the external deficit and allow for lower interest rates, deterring some of the flightier forms of capital. It would be all the more desirable because the budget deficit, at 1.4% of GDP last year, was flattered by windfall revenues from the credit-fuelled boom in domestic demand.Sadly, the appetite for this sort of policy seems limited. With many of Turkey’s big export markets struggling, there is a reluctance to curb domestic demand. Harvard’s Mr Rodrik fears a loss of Turkey’s post-2001 discipline and a reversion to the sort of crowd-pleasing economic policies that led to trouble in the 1980s and 1990s.Storing up strainsThe wobbles at the end of last year, which depleted Turkey’s shallow pool of currency reserves, ought to have been a warning about the dangers of relying on foreign capital and the need to insure against its drying up. The risk then was of a sudden and protracted stop in foreign-capital flows, which would have meant a hard landing for Turkey’s economy. But the European Central Bank’s huge provision of cash to euro-zone banks has led to a revival in risk appetite, which has kept capital flowing to Turkey and elsewhere. That has lessened the pressure for prudence.The danger now is that a few more years of big current-account deficits, and the debt-creating capital flows that finance them, will leave Turkey less resilient when trouble strikes. Few countries that run big external deficits have avoided subsequent stresses. You don’t need to stand atop the Galata tower to see problems ahead.

InfoGnomon

In this section»Istanbuls and bearsClear and present dangerAll that glistersThe Wenzhou experimentBook-cooking guideFrom Brussels, with shoveHistorysisMarjorie Deane internshipsReprintsRelated topicsBusinessEmerging marketsMonetary PolicyPolitical policyEconomic policyBustling below is a city of 15m that lies at the heart of one of the world’s fastest-growing economies. Figures released on April 2nd showed that Turkey’s GDP rose by 8.5% in 2011 after a 9% increase in 2010 (see chart 1)

ΦΩΤΟΓΡΑΦΙΕΣ

ΜΟΙΡΑΣΤΕΙΤΕ

ΔΕΙΤΕ ΑΚΟΜΑ

ΠΡΟΗΓΟΥΜΕΝΟ ΑΡΘΡΟ

ΥΠΕΡΨΗΦΙΣΤΗΚΕ Η ΡΥΘΜΙΣΗ ΓΙΑ ΤΗ SIEMENS

ΕΠΟΜΕΝΟ ΑΡΘΡΟ

Λάθος χώρα για αυτοκτονία

ΣΧΟΛΙΑΣΤΕ